米国株式投資のシステムトレードプラットフォームである 「Quantopian」 を使用してPythonで売買アルゴリズムを開発します。

トレーディングアルゴリズムを1つの「Factor(指標)」のみで構築する事は稀です。

このページでは、「Pipeline」の「Factor」の応用例として、合成ファクターを作成する方法について解説します。

Pipelineで出来ること

Pipelineの基礎については、以下のページを参考にして下さい。

「Pipeline」を定義して実行

株価の終値の「10日移動平均」、「30日移動平均」、「(10日移動平均+30日移動平均)/ 2」を返すPipelineを定義し、実行します。

#ライブラリのインポート

from quantopian.pipeline import Pipeline

from quantopian.research import run_pipeline

from quantopian.pipeline.data.builtin import USEquityPricing

from quantopian.pipeline.factors import SimpleMovingAverage

#パイプライン定義

def make_pipeline():

mean_close_10 = SimpleMovingAverage(inputs=[USEquityPricing.close], window_length=10)#10日移動平均

mean_close_30 = SimpleMovingAverage(inputs=[USEquityPricing.close], window_length=30)#30日移動平均

#合成ファクター =(10日移動平均+30日移動平均) / 2

combine_mean = (mean_close_10 + mean_close_30) / 2

return Pipeline(

columns={

'mean_close_10': mean_close_10,

'mean_close_30': mean_close_30,

'combine_mean': combine_mean

}

)

#パイプラインの実行

result = run_pipeline(make_pipeline(), '2019-05-01', '2019-05-01')

#結果を表示

result.head()

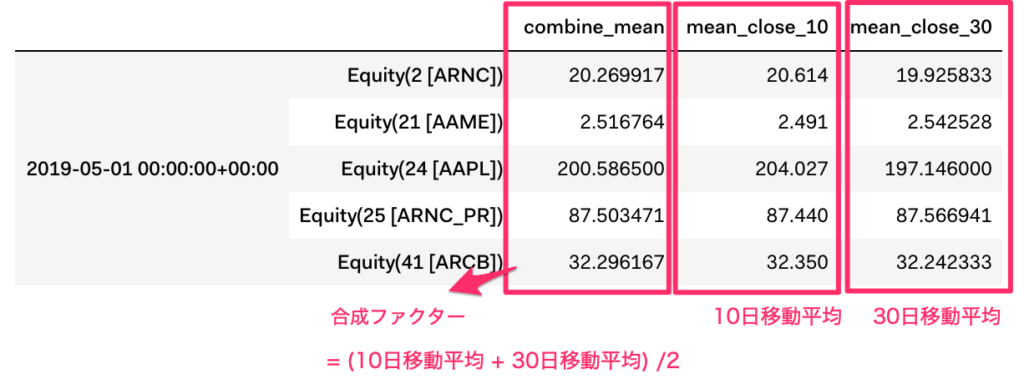

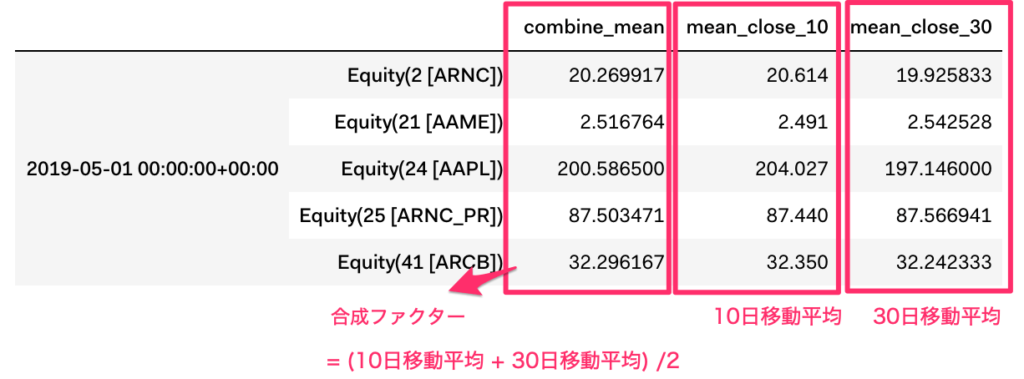

実行結果

「10日移動平均」、「30日移動平均」、「(10日移動平均+30日移動平均)/ 2」をインデックスとした「DataFrame」が表示されます。

解説

簡単に、コードの解説をします。

必要なモジュールのインポート

まず、「Pipeline」作成に必要なモジュールをインポートします。

#ライブラリのインポート from quantopian.pipeline import Pipeline from quantopian.research import run_pipeline from quantopian.pipeline.data.builtin import USEquityPricing from quantopian.pipeline.factors import SimpleMovingAverage

Pipelineの定義

「pipeline」の定義をしています。

def make_pipeline():

mean_close_10 = SimpleMovingAverage(inputs=[USEquityPricing.close], window_length=10)#10日移動平均

mean_close_30 = SimpleMovingAverage(inputs=[USEquityPricing.close], window_length=30)#30日移動平均

#合成ファクター =(10日移動平均+30日移動平均) / 2

combine_mean = (mean_close_10 + mean_close_30) / 2

return Pipeline(

columns={

'mean_close_10': mean_close_10,

'mean_close_30': mean_close_30,

'combine_mean': combine_mean

}

)

10日移動平均の計算

「SimpleMovingAverage」関数を使用して、10日移動平均を計算しています。

mean_close_10 = SimpleMovingAverage(inputs=[USEquityPricing.close], window_length=10)#10日移動平均

合成ファクターの計算

「(10日移動平均+30日移動平均)/ 2」の合成ファクターを定義しています。

#合成ファクター =(10日移動平均+30日移動平均) / 2

combine_mean = (mean_close_10 + mean_close_30) / 2

Pipelineの実行

最後に、Pipelineを実行します。実行には、「run_pipeline」をインポートする必要があります。

「make_pipeline」を「2019-5-1」から「2019-5-1」の期間で実行します。

#Pipelineの実行 from quantopian.research import run_pipeline #パイプラインの実行 result = run_pipeline(make_pipeline(), '2019-05-01', '2019-05-01')

結果を表示

Pipelineを実行した結果の先頭5行を表示します。

#結果を表示 result.head()

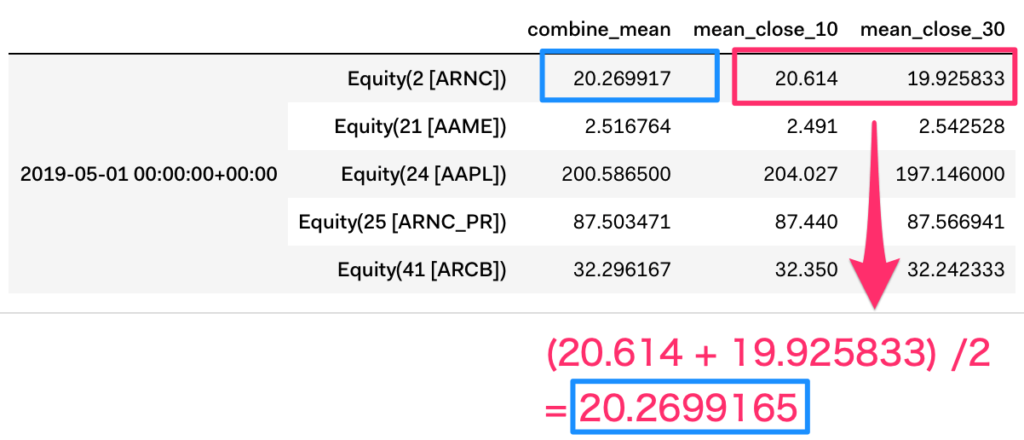

検証

Pipelineを実行した結果から、「合成ファクター」が定義通りに正しく計算されている事がわかります。

参考ページ(公式チュートリアル)

「Quantopian」学習のオススメ講座

「Python for Financial Analysis and Algorithmic Trading 」は、Pythonで金融分析やアルゴリズムトレーディングを作成するための講座です。

世界的に有名なUdemy講師であるJose氏が、「Quontopian」について動画で解説している稀有な講座です。

例えば、「ボリンジャーバンド」を活用したトレーディングアルゴリズムを作成する事が出来ます。